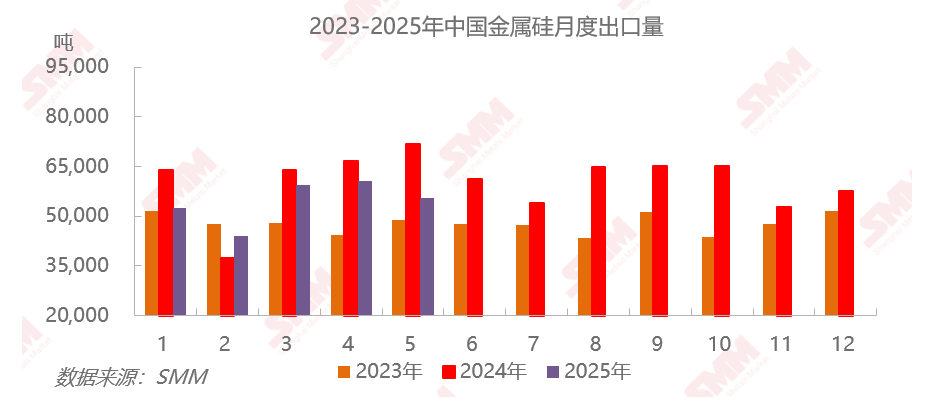

SMM News on June 23: According to customs data, exports: In May 2025, silicon metal exports stood at 55,700 mt, down 8% MoM and 22% YoY. From January to May 2025, cumulative silicon metal exports reached 272,400 mt, a 10% decrease YoY. Imports: In May 2025, silicon metal imports were minimal, less than 4 mt. Cumulative imports from January to May 2025 amounted to 5,200 mt, a 55% decrease YoY.

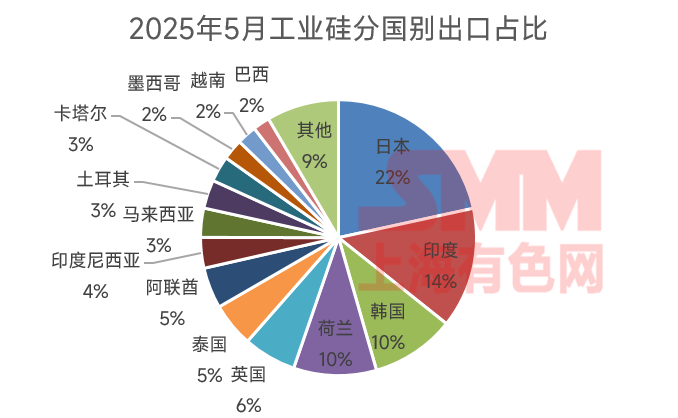

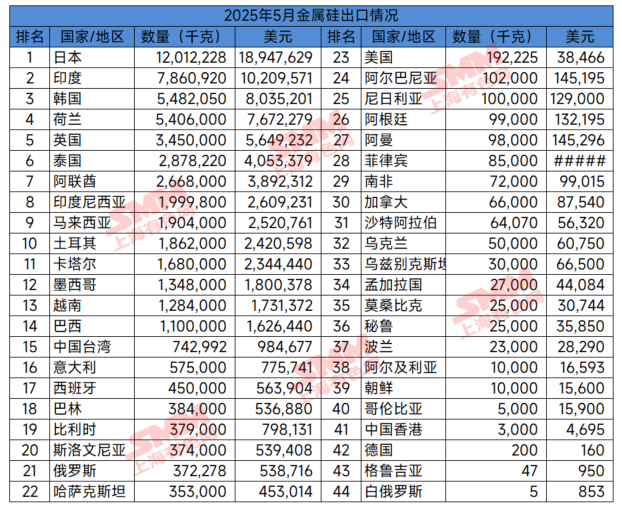

In terms of exports, a total of 44 countries or regions were exported to in May. The top 10 export destinations accounted for 81.8% of total exports, with a volume of 46,000 mt. The top five export destinations accounted for 61.5% of total exports, with a volume of 34,000 mt. The rankings were as follows: Japan (12,000 mt), India (7,900 mt), South Korea (5,500 mt), the Netherlands (5,400 mt), and Thailand (2,900 mt). From the perspective of consumption share, exports accounted for approximately 16% of total silicon metal consumption in May, an increase of 1 percentage point YoY, primarily due to a decline in domestic polysilicon sector consumption.

Silicon metal exports declined both MoM and YoY in May. On one hand, some overseas users reduced the frequency of tenders and procurement volumes, leading to a YoY decline in demand. On the other hand, factors such as invoicing issues led some exporters to raise quotes or delay shipments, affecting monthly export volumes. With the impact gradually weakening, silicon metal exports are expected to recover MoM in June.

For more detailed market information and dynamics, or other information needs, please call 021-51666820.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)